Key Summary: UK and Nordic inflation have fallen sharply from 2022 peaks but began to diverge in early 2025. By mid-2025, UK CPI inflation is again above target (~3½ %), while Sweden’s and Finland’s inflation is near zero. Major structural drivers include past energy shocks, labour market tightness, supply‑side constraints, and exchange‑rate movements. Nordic economies have generally lower energy cost exposure and stronger safety nets, leading to gentler disinflation. The analysis underscores the need for policy coordination: prudent monetary policy to anchor expectations, targeted support for households, and structural reforms to raise productivity and labour supply. Altrom Centre’s independent review stresses that understanding these structural differences is vital for sustainable price stability across regions.

Recent Inflation Developments

Since 2022, inflation rates in the UK and the Nordic region have trended sharply downward from multi‑decade highs. In the UK, CPI inflation peaked above 11% in late 2022. By late 2024 it had fallen to about 2½ % (CPI, Dec 2024). However, by Q2 2025 the UK inflation rate began edging up again: CPI rose to 3.5% in the 12 months to April 2025 (from 2.6% in March). This uptick reflects temporary base effects (e.g. higher energy and utility bills) that the Bank of England (BoE) had anticipated. The BoE projects inflation will peak near 3.7% in the first half of 2025 before falling back to 2%.

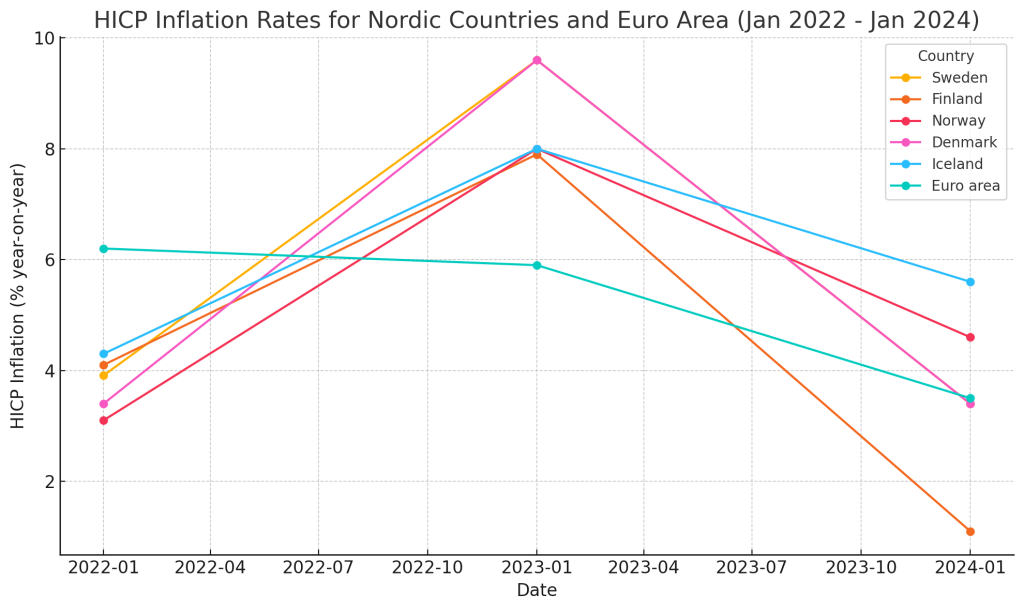

In contrast, Nordic inflation has largely subsided to near-zero levels. For example, as of April 2025 Sweden’s CPI was 0.3%, and its CPIF (CPI with fixed interest) 2.3%. Finland’s CPI inflation was 0.5% in April. In Norway, CPI inflation was 2.5% (April), and in Denmark, HICP inflation was 1.5% (April). Even Iceland – often included in Nordic analyses – saw inflation around 3–4% by mid-2025. Figure 1 illustrates that all five Nordic economies saw inflation tumble from late‑2022 peaks (often 5–9%) to very low levels in early 2024, with further declines by 2025 in most countries. (For comparison, the EU27 average was ~2% in spring 2025.)

Figure 1: Consumer-price inflation in Nordic countries and the EU (HICP, % year‑on‑year). Inflation spikes in 2022 (left) give way to broad disinflation through 2024. By Jan 2024, Swedish inflation was ~3.4%, Finnish ~1.1%, Norwegian ~4.6%, Danish ~0.9%, Icelandic ~5.6%. All curves have since converged toward low single digits.

Comparing UK and Nordic Inflation

The post-2024 gap between UK and Nordic inflation reflects different exposures and policy paths. The UK’s higher current inflation is driven partly by larger past rises in energy, food and housing costs, and by renewed price pressures in services. BoE data note that household energy bills are “around 25% lower than their recent peaks” by 2025, yet still contribute significantly to inflation because of earlier hikes. Food inflation in the UK fell from ~20% in 2023 to ~2% by end‑2024, but rent, services and wage-driven costs have kept core inflation above 3%.

In the Nordics, much of the energy shock passed earlier and energy prices were partly stabilized by domestic renewables (hydro, wind) and government rebates. Food inflation in Scandinavia also eased to very low levels by 2024. As a result, core inflation in Nordics is now mostly a percent or less (Sweden’s CPI excluding food & energy was ~0.9% in April), whereas UK core inflation remains stubbornly higher.

Another factor is currency and external price transmission. The British pound weakened against the euro in 2022–24, so imported inflation (from Eurozone suppliers) stayed elevated. By contrast, the Norwegian krone’s brief 2022 weakness ended, and Nordic inflation expectations remain well-anchored. The EU’s near‑term inflation (Euro area ~2% in early 2025) feeds into both UK and Nordic prices, but the UK’s exchange rate dilution means imported goods cost more.

Labour markets have been tight across all these economies, fueling wage growth. However, the Nordic model of coordinated wage bargaining has kept wage rises moderate and nearly in line with productivity. For example, Sweden expects average wage growth of ~3.5% in 2024, in line with its ~2% inflation, limiting “second-round” wage effects. Denmark and Norway similarly report modest wage agreements. In the UK, the tight labour market also spurred above-target wage growth, but inflation-indexing of some costs (like regulated utility rates) has amplified effects.

Fiscal policy also plays a role. After pandemic stimulus, many Nordic governments ran conservative budgets and provided targeted help (e.g. capped energy bills). The UK delayed some fiscal tightening, and tax thresholds were frozen in 2024, which can entrench inflation. The IMF and OECD have noted that remaining fiscal support in the UK could slow disinflation, whereas more restrictive policy is appropriate. All else equal, tighter UK fiscal policy (via lower spending or higher taxes) and carefully calibrated social support will help lower inflation sustainably.

Structural Drivers of Inflation

The “structural drivers” of inflation refer to underlying supply-and-demand conditions that persist beyond any single price shock. Key structural factors now include:

- Energy and commodity markets: Many Nordic economies have substantial renewable electricity or domestic oil/gas (Norway/Iceland), insulating them somewhat from global oil/gas swings. The UK remains dependent on world fossil fuel prices, and although UK wholesale gas costs plunged from the 2022 peak, they stayed above pre‑2021 levels, keeping a floor on inflation. Global oil price rises in 2024 (to around $80–90/barrel) contributed to UK service costs (transport, fuels) and also modestly lifted Nordic inflation via gasoline. Overall though, energy is no longer the primary driver; it is transition-related costs (carbon pricing) and earlier steep hikes that persist in inflation indices.

- Supply constraints and production bottlenecks: Both regions faced pandemic-era supply disruptions, but these largely eased by 2024. However, sectors like housing (new builds) have long lags. UK housing shortages (and rising rent and mortgage costs) are partly structural and keep inflation above target. Nordic housing markets are also tight (especially in cities), but large social housing stocks and stabilizing construction help contain housing inflation. Global supply-chain shifts (reshoring efforts, tech deficits) have slightly limited availability of machinery/components, adding general cost pressure, but these effects are relatively similar across Europe.

- Labour market and demographics: Aging workforces mean labour shortages are structural. The UK’s departure from the EU (Brexit) led to permanently smaller low‑wage labour supply in services and care, pushing up wages in those sectors. Nordic countries have aging populations too, but robust immigration policies and active labour programs help keep labour supply growing. Denmark and Norway report tight labour markets but increasing participation; Sweden has room to raise the retirement age further. Structural skill mismatches (e.g. green energy requiring new skills) may cause localized inflation in wages, but all central banks expect labour pressures to ease as economies slow slightly.

- Regulation and taxation: In the UK, rising regulatory costs (e.g. higher national insurance contributions, green levies on power) are built into prices. Nordic countries often internalize externalities more gradually and have more predictable rules. For instance, Sweden’s carbon tax and EU‑ETS costs are long‑established and anticipated by businesses, whereas UK energy price guarantees (2022‑23) created sharp fiscal ends and resumed full pricing by 2024, causing a recent jump in utility bills. Changes in VAT or other taxes on goods/services can also cause one‑off inflation spikes; policy in both regions has been cautious to avoid fueling lasting inflation.

- Exchange rates: As noted, currency swings have structural effects. The pound’s weakness (from mid-2022 through 2023) imported inflation; from mid-2024 it modestly recovered, which will dampen some imported price pressures. The Swedish krona and Norwegian krone have been relatively stronger (Norwegian krone even hit multi-year highs), which eases imported cost burdens. Currency volatility is a structural risk (e.g. if the krona weakens again, Sweden could see higher import inflation despite low domestic pressure).

Overall, inflation is now shaped more by these underlying factors than by pure momentum. The Bank of England observes that the main shocks (energy, food) have “receded” and monetary policy has helped reduce second-round effects. Likewise, the Nordic central banks (Riksbank, Norges Bank) note inflation near target or declining, reflecting that structural pressures (e.g. wage increases) are smaller than two years ago.

Policy Implications

These trends imply different policy challenges:

- Monetary policy: The Bank of England paused hikes as inflation fell, but faces renewed upward pressure. Maintaining the official rate sufficiently high to ensure inflation returns fully to 2% is crucial. In practice, this means being ready to delay cuts or even tighten if inflation lingers. Nordic central banks (Sweden, Norway, Denmark) are likely to begin cutting rates in mid‑2025 as inflation is largely on target and to preempt deflation risks. In each case, central banks must communicate clearly to keep inflation expectations anchored.

- Fiscal policy: Governments should avoid large deficit-financed stimulus when inflation is above target. The UK’s recently announced measures (water bill relief, household support) should be temporary and targeted to the most vulnerable, to avoid reigniting broad demand. In Nordics, small fiscal support has been sufficient. Longer term, reforms to improve labour supply (e.g. childcare support, training) and raise productivity (digitalization, infrastructure) can ease inflation pressures without hurting growth.

- Structural reforms: Key are measures to increase supply. For the UK, housing supply reform (planning reforms, rental sector incentives) would reduce housing cost inflation. Improving energy efficiency in housing can buffer households from fuel cost swings. Both regions would benefit from investing in skills to meet green transition demands, ensuring new industries do not bottleneck on labour.

- Regional coordination: The Altrom Centre’s independent analysis stresses that cross-country collaboration is valuable. For example, common carbon pricing (EU‑ETS linking with UK/Nordic schemes) could reduce arbitrary cost differentials that distort trade. Joint procurement (e.g. for renewables or hydrogen infrastructure) can lower costs. Sharing data and research (on, say, energy demand or labour trends) can help tailor policies.

In conclusion, inflation in the UK and Nordics is retreating from its highs but remains sensitive to structural factors. The UK is experiencing a transitory bounce in 2025, whereas the Nordic countries enjoy mostly benign inflation. The strategic lesson is that monetary policy must remain vigilant, and fiscal/structural policies should bolster supply capacity. Altrom Centre’s commitment to Excellence and Independence underpins this evidence-based review, which aims to inform collaborative policymaking across the region and support the Impact-oriented goal of stable, equitable economies.