Key Summary: The EU’s Carbon Border Adjustment Mechanism (CBAM) – a tax on embedded CO₂ in key imports – is reshaping trade for steel, cement, fertilizers, aluminium and power. By Jan 2026 (after a transition phase), CBAM will require importers to buy carbon certificates aligned with EU carbon costs. This protects EU producers but imposes new costs on exporters, especially in developing markets. Studies estimate large impacts: e.g. India’s steel exports to the EU could face a duty ~16% of value. Low-income exporters (e.g. in Africa) are projected to see their exports fall by ~6%, with GDP declines around 1–2%. Policymakers in emerging markets must respond through industrial decarbonization, diplomatic negotiations, and adaptation of trade policies.

Altrom Centre’s analysis highlights that while CBAM can incentivize global green tech uptake, careful multilateral design is needed to avoid regressive effects on vulnerable economies.

What is CBAM and Who It Covers

A Carbon Border Adjustment Mechanism is essentially a carbon tax on imports. The EU’s CBAM, part of the European Green Deal, will “apply an EU-equivalent carbon price on imports” of carbon-intensive goods. It seeks to prevent “carbon leakage” (firms relocating to unregulated markets) by equalizing carbon costs for EU and non-EU producers. After an initial reporting-only phase (Oct 2023–Dec 2025), a full CBAM will start 1 Jan 2026. Importers of covered goods will purchase CBAM certificates proportional to the embedded CO₂ in each shipment.

The initial sectors covered include iron & steel, cement, fertilizers, aluminium, and electricity. (Hydrogen may be added later.) Together these account for a large share of the EU’s carbon imports. For example, steel and aluminum from Türkiye, China and India, and power from Russia, are major inputs into EU industry. The scheme’s scope will expand gradually – the EU plans to extend CBAM to chemicals and possibly other sectors over time. Crucially, imports face these duties unless the exporting country has an equivalent carbon pricing. This makes CBAM both an environmental tool and a trade policy instrument.

Potential Costs for Emerging Markets

CBAM’s economic impact on emerging markets has been quantified in recent studies. One analysis finds that if EU free allowances under its emissions trading system were fully phased out (100% CBAM coverage), the implied carbon duty per tonne of exports to the EU would be very high – roughly €150/tCO₂ for Chinese steel exports, €174/tCO₂ for India, €169/tCO₂ for Russia, €60/tCO₂ for Türkiye and €66/tCO₂ for the USA. In other words, an Indian steel shipment to Europe could face an extra charge equal to 16% of its 2022 value. For aluminium, India’s exports (25% going to EU) would incur about €20 per tonne, whereas China’s (14% to EU) would pay ~€11 per tonne.

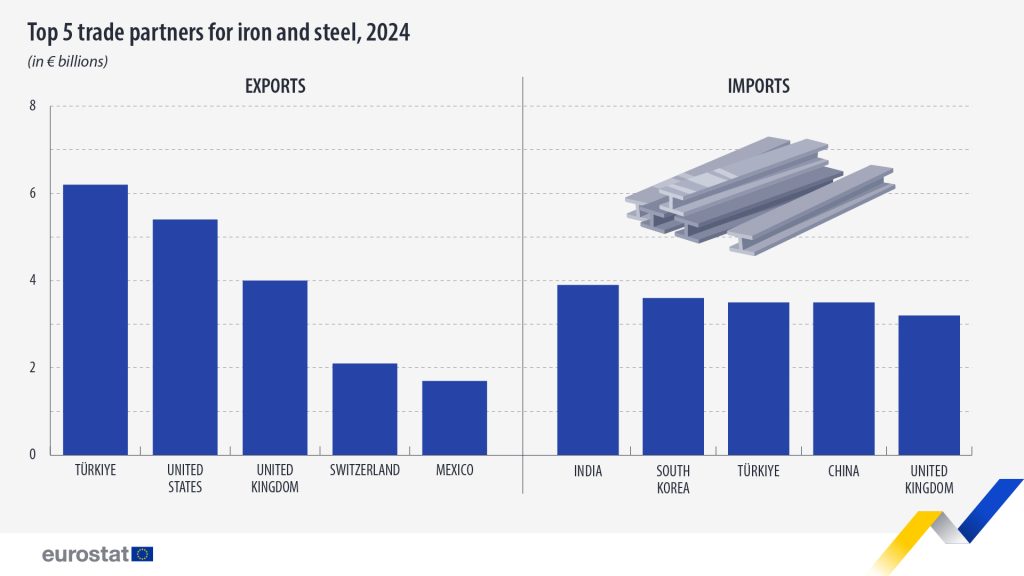

Figure: EU27 imports of CBAM-covered goods by leading exporters (left) and share of those exports going to EU markets (right). Developing countries like Türkiye, India and China export large volumes of steel/aluminium to the EU. The right chart shows that EU demand accounts for ~60% of Turkish aluminium exports and ~37–33% of Indian iron & steel exports – implying these sectors are highly exposed to CBAM charges.

Several immediate impacts on emerging economies follow. The most direct effect is higher costs for exporters in CBAM sectors. Our industry may try to absorb these costs (squeezing margins) or pass them on by raising prices, potentially losing market share. For relatively clean producers (lower carbon per unit), the competitive hit is smaller; countries with lax energy policies face higher effective tariffs. A World Bank “exposure index” confirms that India (23.5% of its steel exports to EU) and Kazakhstan (3.9%) are most exposed in steel, while Russian power (73% to EU) and Belarusian cement (34%) are critical cases.

Econometric modelling indicates broader trade and growth effects. With CBAM applied globally, low- and middle-income exporters suffer disproportionately. One forecast suggests EU CBAM could cut Africa’s exports by ~5.7% and lower its GDP by several percentage points. For example, Mozambique’s GDP might fall ~1.6% due to CBAM impacts on its aluminium and mineral exports. Smaller economies like Zimbabwe, Albania or Bosnia (with export mixes heavy in metals/fertilizers) may see output declines. In India, CBAM might reduce steel output or exports (already facing competition from China) unless offset by higher domestic carbon pricing.

Even non-intensive sectors feel indirect impacts. A carbon price on inputs (cement, steel) raises construction costs and inflation, eroding real incomes. There is also the risk of trade diversion: some exports shift from the EU to other markets (e.g. China, US), but these markets may not fully absorb the redirected goods. This can hurt commodity prices globally, which is mixed for producers (lower prices) and consumers (cheaper imports).

Strategic Responses and Policy Options

Emerging economies have limited choices but must plan responses along several lines. An ECDPM study outlines four strategies: decarbonize, emulate, challenge, or avoid. The most feasible and sustainable is to decarbonize domestic industry. This involves investing in cleaner technology so that exports carry lower carbon content and thus incur smaller CBAM fees. For instance, steelmakers in India or Brazil could adopt hydrogen-based or electric arc furnace processes (as in Europe) to lower embedded emissions. Over the long run, aligning with global climate norms may open new low-carbon markets.

Second, countries can “emulate” EU policies by establishing their own carbon pricing (tax or trading schemes). If a country’s carbon price matches the EU’s, its exports could avoid CBAM duties. This requires robust domestic policy, but several emerging markets (China, South Korea, Mexico) are exploring national ETS or carbon taxes. Even partial alignment (sectoral carbon pricing) helps: for example, if India imposes a steel carbon fee, Indian steel exporters might receive CBAM rebates.

Third, nations should challenge unilateral measures diplomatically. Many developing countries (India, South Africa, etc.) have voiced concerns at the WTO, arguing CBAM must account for different national circumstances and climate responsibilities. They can seek technical adjustments (e.g. excluding embedded emissions from legacy investments) or revenue recycling arrangements. Coordinating a multilateral framework (through G20/UN) could yield a more equitable global carbon border system.

Finally, policymakers must adapt trade and industrial policies. This includes diversifying export markets (reducing reliance on EU markets vulnerable to CBAM). It also means seeking climate finance and technology transfer to support green industrialization. Some emerging manufacturers may shift away from carbon-intensive exports to greener sectors (electronics, services, agriculture).

For firms, measures include improving energy efficiency, sourcing renewable power, and calculating carbon footprints accurately (to minimize liability). Governments may offer subsidies or loan guarantees for “CBAM-proof” investments (e.g. new refineries, cement kilns). They may also negotiate bilateral deals: for example, if the EU links CBAM to India’s proposed carbon market, Indian exports to the EU could be exempted.

The key message from our evidence-based review is that CBAM raises the stakes of industrial transition for emerging markets. It effectively extends the EU’s climate policy globally. This can be a catalyst for green investment – for example, an Indian steel producer that internalizes the carbon price may innovate and gain tech leadership. But it can also be punitive if imposed without support. Hence, Altrom Centre emphasizes collaboration: technical assistance programs, carbon credit recognition, and phased implementation (CBAM itself has a multi-year roll-out) can mitigate shocks.

Economic Projections and Estimates

Several high-quality studies quantify the CBAM effect:

- The cited analysis shows specific duties on major exporters. It found that under 100% coverage, China, India and Russia would face ~€150–174/tonne, translating into 7–16% of 2022 steel values for India’s exports. These are not trivial costs, especially for price-sensitive commodity exports. Importantly, the study notes that in some cases (e.g. US and India steel), even with CBAM, these countries might retain some competitive edge, implying partial rather than total transmission of costs.

- The World Bank’s CBAM Exposure Index (public dashboard) identifies dozens of vulnerable economies. For iron & steel, India ranks highest (23.5% of exports to EU). For electricity, Russia stands out (73% to EU). Such metrics help countries prioritize reforms.

- Macroeconomic models (e.g. from the LSE/African Climate Foundation) project that an expanded CBAM could reduce GDP in affected nations by ~1–2%. For sub-Saharan Africa as a whole, exports fall ~5.7%. These models also find some export diversion (Africa may export more steel to India/China), but not enough to offset losses. Crucially, sectors like mining and metals (important for government revenue and jobs) would take the hit.

In sum, while EU producers gain competitiveness, many emerging economies would face non-negligible headwinds from CBAM. This underscores the advice of global institutions: use CBAM revenues to assist transition. For example, if the EU recycles CBAM proceeds into technology transfer funds for poorer countries, the negative impact could be softened.

Mitigation

CBAM is a landmark policy linking climate action to trade. By January 2026 it will rewire global value chains in carbon‑intensive goods. Our analysis, in the spirit of Altrom Centre’s Excellence and Independence, draws on empirical studies to show that emerging markets will face real economic costs. The strategic policy implication is twofold: (1) Mitigate impacts through multilateral cooperation, technology support, and adaptation measures; (2) Accelerate domestic decarbonization and innovation to turn CBAM from a burden into an opportunity.

In practice, this means integrating CBAM into broader green industrial strategies: investing in clean energy, refining production processes, and seeking mutually agreeable international frameworks. The aim is to transform CBAM from a divisive trade issue into a catalyst for global low-carbon growth, consistent with the Centre’s Collaboration and Impact values.