Key Summary

- Supply Chain Diversification: Businesses and governments are actively seeking to reduce dependence on any single country by nearshoring and building redundant supply lines. Rising calls for a “China + 1” strategy exemplify this trend.

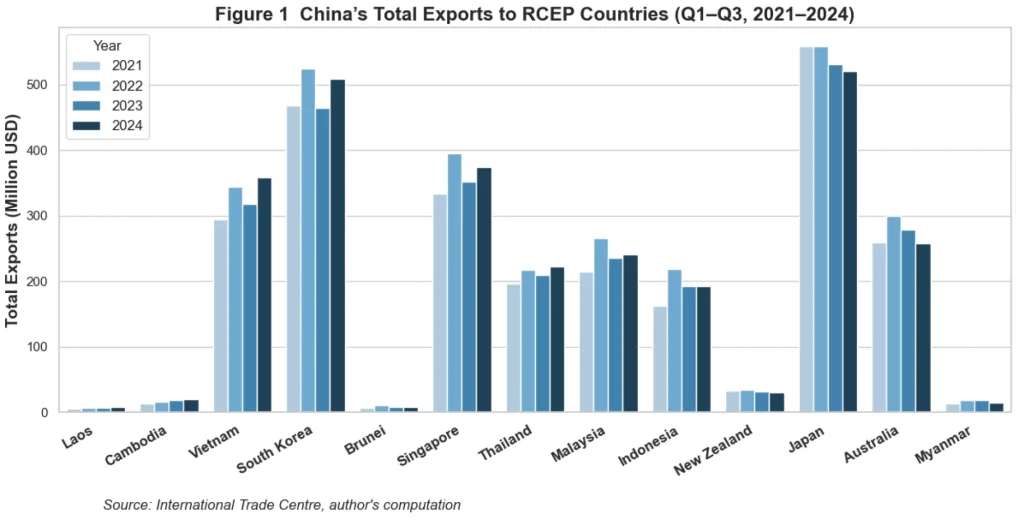

- Regional Trade Agreements: In the face of multilateral tension, regional blocs are gaining importance. For example, intra-ASEAN trade under RCEP jumped over 7% in 2024, demonstrating the pact’s stabilizing role. Newly activated trade deals (e.g. UK–Pacific, EU–Asia) are diversifying markets.

- Trade Facilitation: Efforts to streamline customs, digitalize documents, and improve infrastructure are underway globally. Such measures aim to cushion the impact of tariffs by lowering non-tariff frictions.

- Adaptation in Industry: Manufacturers are redesigning products for modular sourcing, and expanding home production capacity. Energy-intensive sectors particularly explore shifting operations closer to end markets to avoid shipping bottlenecks.

- Growth Headwinds: Despite adaptive measures, slower trade growth is expected. IMF data projects global trade volume to underperform GDP for a second year, reflecting caution.

The New Trade Landscape

Global trade flows are being rewired. Even before the 2025 tariff surge, analysts observed a gradual deglobalization trend: companies stockpiled inputs during COVID, spurring relocation of factories. Now, tariffs have accelerated this. As the World Economic Forum notes, many governments and firms are adopting a “China + 1” posture. This means sourcing components through a second country (often in Southeast Asia or Latin America) to complement Chinese supply. For instance, Japanese auto makers are expanding plants in Vietnam and Mexico; semiconductor producers are funding foundries in Taiwan, India and Europe. Such moves reduce single-point-of-failure risk: if one country’s exports are taxed or blocked, goods can still flow via alternative routes.

Regional Trade and Bilateral Deals

Regional pacts and alliances are providing some stability. The Regional Comprehensive Economic Partnership (RCEP), an Asia-Pacific free-trade area, began to show effects: after a brief dip, intra-ASEAN trade grew by over 7% in 2024. Other agreements are also evolving.

The UK, for example, activated a trade deal with Pacific nations (CPTPP) and signed new tech-sector agreements with South Korea and India. The EU is pursuing deals with India and Mercosur. These initiatives are meant to sidestep rising US tariffs. On the U.S. side, moves like negotiating new “indigenous electronics” rules and reassessing NAFTA (USMCA) content standards reflect attempts to keep regional supply chains intact. However, the proliferation of overlapping rules can increase complexity: companies now often need to navigate different origin rules for parallel markets.

Supply Chain Policies and Resilience

Governments are rolling out strategies to bolster supply-chain resilience. The EU, for example, published a “Resilience and Robustness of Supply Chains” plan calling for stockpiling critical goods (pharmaceuticals, semiconductor inputs, rare earths) and encouraging domestic production through subsidies. Similarly, the U.S. and Japan are considering incentives (tax credits, grants) to onshore key industries like electric vehicle batteries. These policies also fund digitalization of customs and logistics. For instance, several countries have accelerated deployment of blockchain tracking for shipments, and streamlined permit processes, to mitigate indirect tariff costs.

Industry is also adapting. Sectors with long lead times (like construction equipment) now often dual-source components and maintain higher inventory levels. Consumer goods companies are redesigning products to use more interchangeable parts. Some firms report paying 5–10% premiums on components to secure backup sources. In parallel, shipping lines are investing in redundant sea lanes, and building capacity in smaller ports to avoid bottlenecks at mega-hubs. These measures aim to spread risk, albeit at a higher cost.

Implications and Outlook

Data suggest that even with diversification, trade growth will lag. The IMF warns that global trade could grow slower than GDP for the foreseeable future. In fact, sustainable bond markets (often a proxy for investment flows) note that trade barriers have “reset” global supply chains – much activity is now about repositioning rather than expanding trade volumes. The Altrom Centre’s research highlights two key takeaways: first, resilience requires open channels of communication.

Countries that maintain some level of trade openness (even with adjusted tariffs) tend to reallocate resources more efficiently. Second, multilateral standards on transparency (for example, a revived WTO monitoring) could reduce uncertainty. In terms of policy, Altrom advises that governments use this moment to strengthen digital trade infrastructure and workforce training – ensuring that supply chains remain flexible enough to absorb shocks, not brittle.

Altrom Analysis

The Altrom Centre concludes that building resilient trade networks is a marathon, not a sprint. Our analysts stress that while short-term measures (like tariff waivers for critical goods) are helpful, the long-term strategy should focus on diversification and collaboration. We suggest forming multilateral working groups on supply-chain security and climate-aligned trade. For investors and policymakers alike, understanding these trends will be crucial to navigate the “new normal” of international commerce.