Key Summary:

- Slowing output: Swedish GDP forecasts were slashed in June – 2025 growth is now ~0.9% vs 1.8% earlier. Norway’s non-oil economy is seen at ~1.8% in 2025. This reflects global trade uncertainty and waning industrial investment in batteries/green steel. However, robust household incomes (Riksbank cited rising real wages) and early rate cuts suggest a recovery may emerge in H2.

- Venture funding & strategy: Nordic VC remains active in niche sectors. In early July Sweden’s Behold Ventures closed a ~$58M fund for game developers. Similarly, a new Nordic Food tech VC fund held a €40M first close for plant-based innovations. These funds signal national strategies: Denmark and Sweden continue to bank on green/tech clusters, while Finland entices investment via a late-April corporate tax cut. State-owned Swedish funds also pivot – e.g. newly, increased allocations to defence tech and renewable infrastructure. Overall, capital flows are concentrating in sustainable industries and AI-enabled services, even as traditional manufacturing attracts caution.

- Policy pivots: Governments are adjusting to headwinds. Finland, facing a 0.8% GDP growth risk, approved major tax cuts and higher deficits to spur investment. Norway’s budget (May 2025) raised petroleum fund withdrawals to support Ukraine aid and cut growth forecasts. Sweden trimmed spending forecasts but left room for private-sector recovery (e.g. robust real wages, energy exports). Importantly, Nordic countries maintain high social investment – Nordic unemployment (~4–6%) is much below EU averages – providing cushions that Southern Europe lacks.

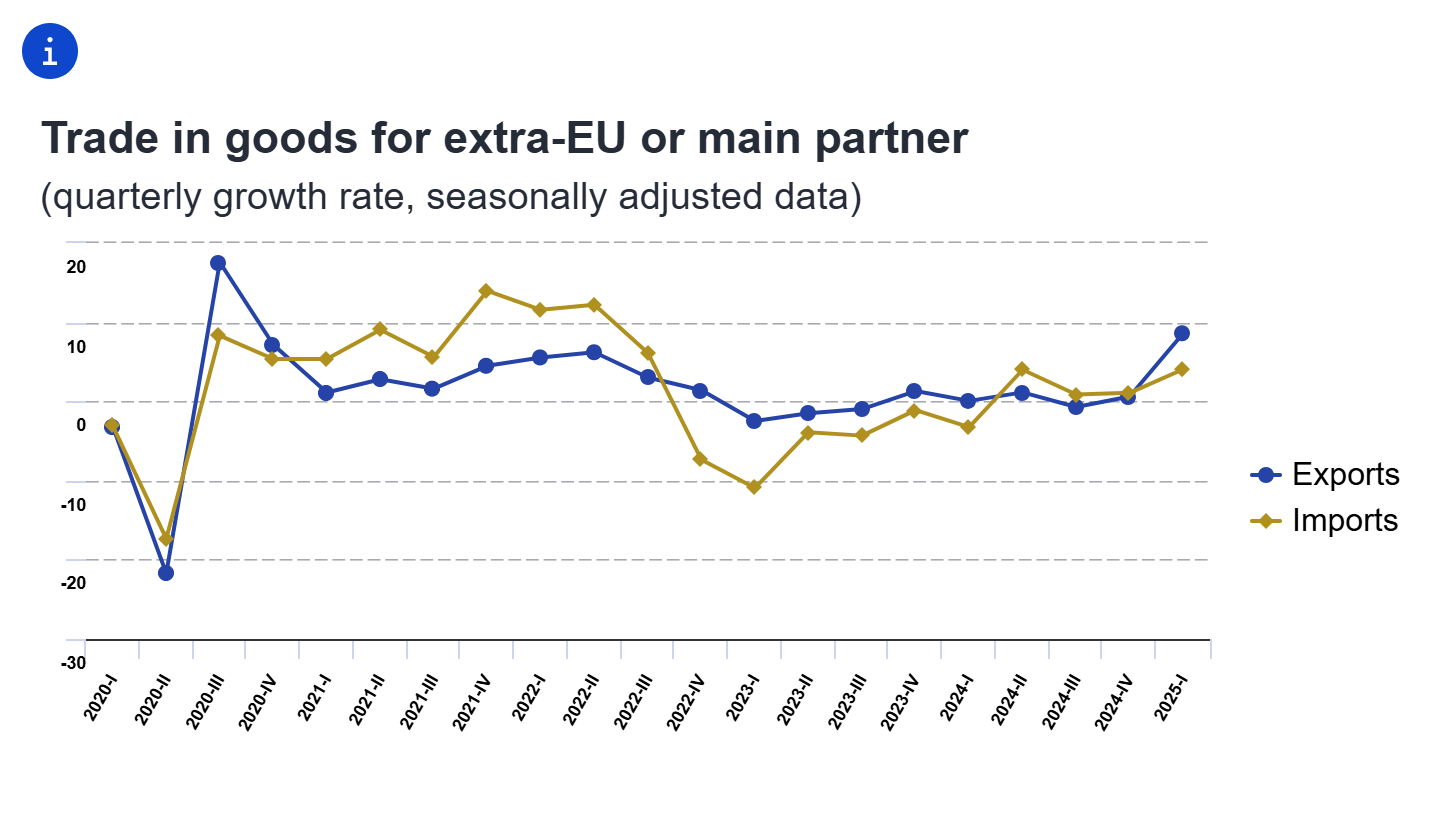

- Trade reorientation: Nordic exporters are diversifying. EU-level data hints Nordics benefit from the same front-loading seen elsewhere: Scandinavian exporters shipped more to the US in Q1 2025 as firms raced Trump’s tariffs. At the same time, Nordic firms are seeking new partnerships: e.g. Finnish industry heavyweights expanding Middle East and African ties, Danish renewable energy firms eyeing the US Inflation Reduction Act markets. Industrial supply chains (electronics, metals) are gradually shifting: while EU exports to China fell, Nordic exports (like Norway’s gas or Sweden’s telecom equipment) remained steadier, partly due to long-term contracts.

Industrial Output and Economic Resilience

Nordic businesses are navigating a crucial inflection point as global headwinds collide with long‑standing strengths in social cohesion, innovation, and trade integration. With industrial output cooling and energy markets shifting, governments and businesses alike are recalibrating policies and investment strategies to maintain competitiveness. From Sweden’s tax reforms to Norway’s expanded trade pacts, this transition phase will determine how the region leverages its green‑tech ambitions and robust welfare systems to thrive in an increasingly fragmented global economy.

Nordic industrial output has plateaued amid global volatility. Sweden’s economy unexpectedly contracted 0.2% in Q1 2025 (q/q) and policymakers halved GDP forecasts. The foreign trade sector is uneasy: Volvo and Scania worry about raw-material bottlenecks, while Finland’s large IT exporters face demand fluctuations. However, domestic cushions help. Sweden’s Riksbank noted rising real wages and falling inflation, expecting consumption to rebound. Similarly, Norway’s economy is buttressed by oil revenues; although non-oil growth is trimmed, unemployment is near record lows. Finland’s baseline was weaker (an industrial slump), but its new government’s stimulus may spark recovery. In sum, measured by output alone the Nordics are cooling off, but strong fundamentals (low debt, solid labor markets) leave them better placed than many peers.

Venture Capital and Strategic Funding

Funding flows reveal strategic bets. In the past week, Swedish venture capital firm Behold Ventures secured $58.2M for a games fund, highlighting Sweden’s ongoing focus on creative tech. Likewise, Nordic Foodtech VC announced a €40M first close for sustainable food startups, reflecting Finland/Denmark’s push into biotech. These rounds parallel larger commitments: Norway’s state pension fund increased green energy allocations, and the European Investment Bank recently opened a Stockholm branch to underwrite Nordic infrastructure.

Notably, high-end AI services are attracting talent: Surge AI’s $15B valuation round (LA-based) does not directly involve Nordics, but Nordic AI labs (e.g. Helsinki-based startups) benefit indirectly from global labeling market shifts. Overall, Nordic investment patterns favor green energy, defense tech, and AI, leveraging government incentives (e.g. Sweden’s clean tech R&D subsidies).

Policy Adjustments and Trade Shifts

National policy is nimble. Finland’s April 2025 budget made it “one of Europe’s most attractive countries for investment” via corporate tax cuts. Defense commitments have also risen (Norway plans ~3% GDP by 2029). Meanwhile, Nordics face the same trade waves as all of Europe. The March 2025 PMI surveys showed Ireland and Spain as EU manufacturing bright spots, but Nordic indices were mixed. Many Nordic firms, especially in high-tech and clean energy, are front-loading exports to the US (e.g. Vestas shipped wind turbines early) ahead of tariffs.

Conversely, Chinese tariffs and slowdowns have had limited direct impact since most Nordic exports are oil/gas, metals, and high-value machinery, where longer contracts hold. Looking ahead, Nordics are positioning for a greener post-surge economy: new hydrogen and battery projects (e.g. Swedish battery “Northvolt” expansions) are slated for 2026, leveraging both EU funds and reoriented trade ties to the US climate sector.

Altrom Insight: The Nordic economies are in transitional mode. Industrial growth has cooled under global headwinds, but robust social safety nets and pro-growth policies (tax cuts, green R&D subsidies) help. Venture funding continues in prioritized sectors like clean energy and AI software. In trade, Nordics remain closely linked to both European markets and new global opportunities, cushioning them from the more extreme swings seen elsewhere. How well they manage policy adaptations and attract capital into sustainable industries will shape their medium-term trajectory