Key Summary:

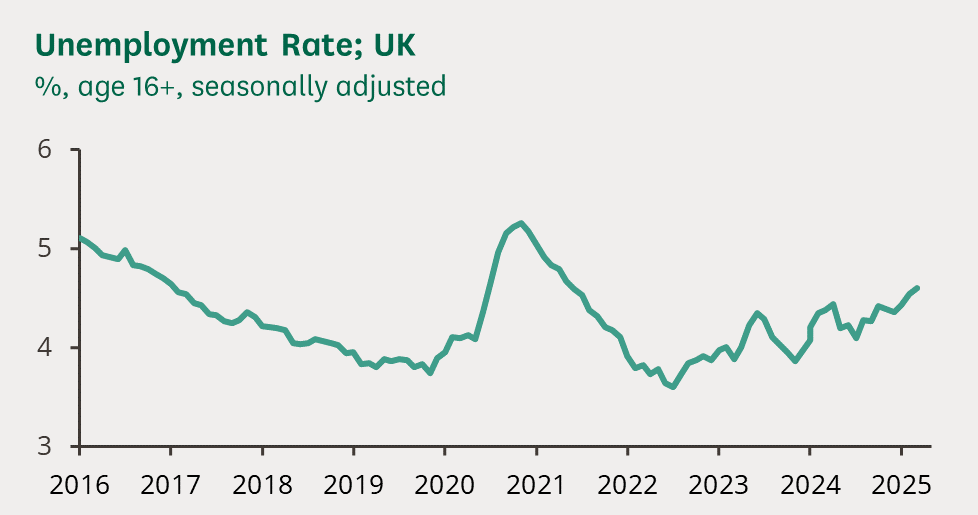

- UK unemployment rate climbed to 4.6% in April (highest since 2021) as economic slowdown takes hold.

- Private-sector regular pay growth slowed to 5.2%, the weakest since late 2024.

- Vacancies fell to 736,000 (four-year low), easing pressure on wages.

- Sterling weakened and rate-cut bets increased on soft labour data.

- Altrom Centre warns that falling labour costs may tempt policymakers to ease monetary policy.

UK Labour Market

LONDON, 12 June 2025 – Britain’s labour market showed clear signs of cooling in recent months, official data revealed this week. The Office for National Statistics (ONS) reported that the unemployment rate rose to 4.6% in the three months to April – the highest since May 2021. At the same time, private-sector wage growth slid to 5.2% (excluding bonuses), its slowest pace since September 2024. Vacancies dropped sharply, down to 736,000 in May (the lowest since early 2021). Investors quickly re‑priced monetary policy: sterling fell and futures markets raised the odds of Bank of England rate cuts later this year.

Altrom Centre perceives that the numbers point to easing inflationary pressure. ‘After a tight labour market for years, we are now seeing unemployment tick up and pay growth decelerate,‘. ‘This slowdown reflects higher taxes and weaker demand – a trend that should temper pay inflation.‘ We highlighted that April’s figures were released after businesses faced a £25bn rise in payroll taxes and a higher minimum wage, factors likely adding strain to firms.

For policymakers, the cooling labour market may shift the outlook on monetary policy. ‘The data strengthens the case for the Bank of England to remain on hold – or even cut rates by year-end – if this trend continues,’. The Bank’s recent guidance that domestic wage growth is now a key signal for inflation decisions. Altrom Centre analysis suggests this labour market easing could keep consumer price inflation on a downward path, though we cautioned that sluggish wage growth may also weigh on spending.

Opposition parties seized on the report’s political implications. Conservative trade spokesman Andrew Griffith blamed recent tax increases and looming regulations for the unemployment rise. Currently, Policymakers on all sides will see these figures as evidence that fiscal drag is biting. Higher unemployment usually reduces wage-push inflation, which should give the Bank more scope to ease monetary policy.

The Altrom Centre emphasises that while near-term inflation is easing, medium-term risks (such as global supply shocks or fiscal shifts) remain. We conclude that “ongoing monitoring is essential. If the labour market softening persists, it could allow for a more supportive monetary stance without stoking inflation, which matters for UK growth.”